A goal of competitive wholesale markets is to be efficient both in the short-run, by ensuring that resources are dispatched to minimize production costs while maintaining secure operations, and in the long-run, by ensuring that market prices help to coordinate investment in new generation or the orderly retirement of resources that are no longer competitive. Across the U.S., annual average wholesale power prices peaked in 2008 and have since dramatically declined—average wholesale prices fell $35–50/MWh between 2008 and 2017 at major trading hubs across the seven organized wholesale markets—followed by an exceptional increase in generator retirements, particularly of coal and nuclear plants. Three main trends over this same period are often considered as contributors to this reduction in wholesale prices: the fall in natural gas prices from the shale-gas revolution, decreasing projections of demand growth due in part to energy efficiency, and the rapid rise of zero-marginal-cost generation with wind and solar.

But did these three trends contribute equally to the decline in wholesale prices, or are some more influential than others? The answer to this question has important policy implications. One could argue that changes in wholesale prices over the past decade are economically efficient if caused primarily by increased competitiveness of natural gas. If instead the price decline was driven primarily by public-policy support for wind and solar, then one could argue that the outcome reflects a market distortion. Generators facing retirement might have an easier time making the case for policy or market-design changes if market distortions rather than competitive pressures were the cause of falling prices.

But did these three trends contribute equally to the decline in wholesale prices, or are some more influential than others? The answer to this question has important policy implications. One could argue that changes in wholesale prices over the past decade are economically efficient if caused primarily by increased competitiveness of natural gas. If instead the price decline was driven primarily by public-policy support for wind and solar, then one could argue that the outcome reflects a market distortion. Generators facing retirement might have an easier time making the case for policy or market-design changes if market distortions rather than competitive pressures were the cause of falling prices.

Impact of Negative Real-Time Electricity Prices on Wholesale Prices

Wind and solar are undoubtedly having some degree of impact on wholesale prices through their contribution to a rise in negative real-time electricity prices, particularly in wind-rich regions of the Midwest, in solar-dominated California, and near wind generators in parts of northern New York and New England (Figure 1). Wind generators that qualify for the federal Production Tax Credit and renewables whose generation contributes to mandatory state renewables portfolio standards have an incentive to continue to generate electricity even when wholesale prices fall below zero.

Overall, however, negative prices reduced average wholesale prices by less than $1/MWh in most regions. Furthermore, most locations at which negative prices significantly reduced average annual prices were near wind, solar, or hydropower plants rather than near other generation types.

Figure 1. Frequency of negative real-time electricity prices in 2019

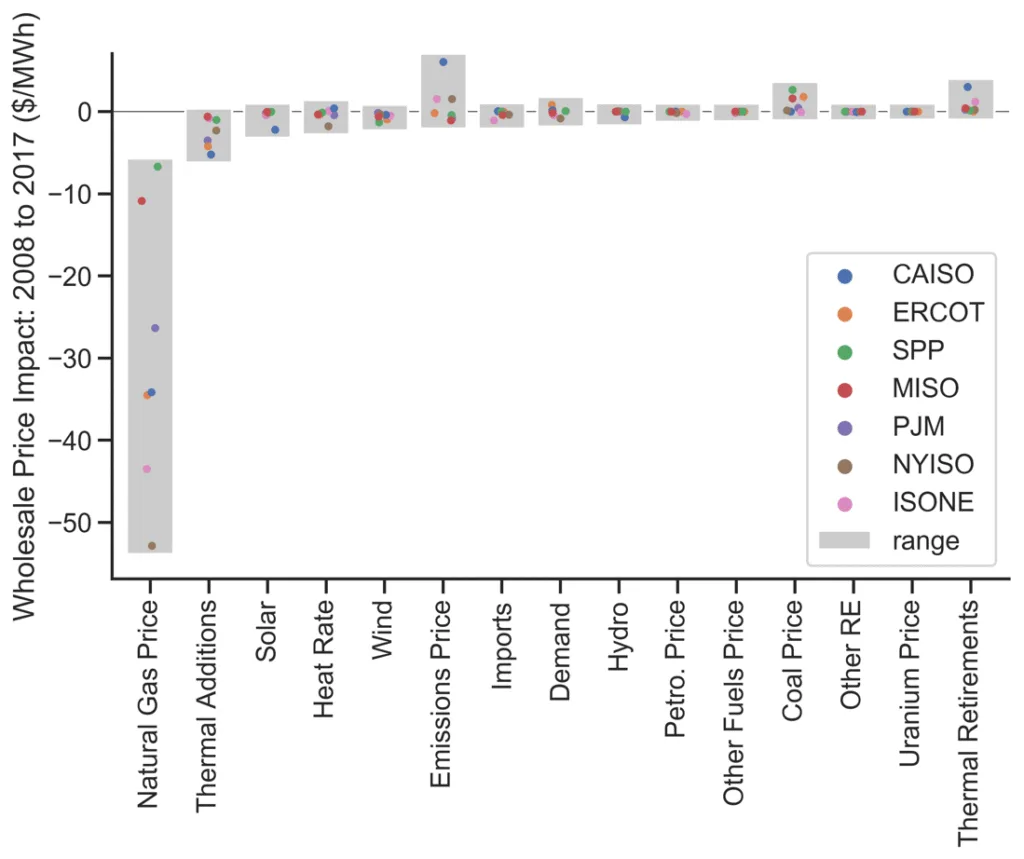

Impact of Natural Gas, Solar, and Wind Prices on Wholesale Prices Since 2008

To quantify the relative contribution of different drivers to this observed decline in wholesale prices, we used a simple supply curve model to estimate hourly prices by intersecting the supply curve with the net demand in each hour (load less variable renewables). The supply curve changed on a daily basis due to natural gas price fluctuations and included historically observed heat rates and capacities of individual generators in each market. With this model, we asked what would be the impact on average annual prices if we changed just one factor at a time between 2008 and 2017 levels?

Our analysis demonstrates that—across all seven organized wholesale markets—changing natural gas prices had the largest impact on wholesale electricity prices between 2008 and 2017, far greater than the impact of wind and solar or any other factor (Figure 2). The decrease in natural gas prices decreased average wholesale electricity prices by $7–11/MWh in the Midwest (SPP and MISO) where coal plants were often marginal generators and $26–53/MWh in the other five regions where gas plants were more likely to be marginal. With low natural gas prices and a relatively flat supply curve in 2017, the impact of growth in wind and solar between 2008 and 2017 on average wholesale prices was less than $3/MWh in all seven markets. The magnitude of the estimated impact primarily depends on the incremental level of wind and solar penetration, where a higher penetration leads to a greater impact on prices.

Figure 2. Average wholesale price impacts of various factors that changed between 2008 and 2017 across all markets

Impact of Wind, Solar, and Natural Gas Prices Going Forward

Using the same modeling approach and future projections from the Energy Information Administration (EIA), we find that natural gas still plays a dominant role, although downward pressure on average wholesale prices from wind and solar deployments increases between 2017 and 2022 for all seven markets. The impacts of wind and solar growth on annual average wholesale prices between 2017 and 2022 particularly stand out in regions where additional wind and solar generation increasingly occurs at times with oversupply conditions driving increased negative prices. Most notable, the projected doubling of solar in California by 2022 in EIA’s Annual Energy Outlook for 2018 may have substantial, non-linear additional impacts on average prices (~$5–7/MWh reduction). Storage and other forms of flexibility not otherwise captured in the supply-curve model may mitigate these impacts. Even with this projected growth in wind and solar, however, changes in natural gas prices remain the dominant price influencer, leading to an expected net increase in average wholesale prices between 2017–2022.

Even with wind and solar penetrations of 40 percent, our more detailed fundamental modeling of markets conducted with LCG Consulting found that high wind and solar penetrations only reduce average prices by $5–16/MWh. At the same time, growth in wind and solar prominently shift the timing and increase the volatility of wholesale prices.

* * *

While impacts are anticipated to increase as wind and solar penetrations grow, our analysis suggests that wind and solar has not been the primary cause of thermal-plant retirements to this point. As such, any policy and market-design changes to slow thermal-plant retirements should be thought-of primary as a reaction to low, market-driven natural gas prices, and not (so far, at least) a consequence of policy-driven renewable deployments. Looking out to the future, we expect that swings in natural gas prices will continue to have a major influence on the average level of wholesale prices, while wind and solar will increasingly drive the timing and volatility of those prices.

Andrew D. Mills

Research Scientist

Lawrence Berkeley National Laboratory